Issue 4 Q4 2025

FEATURING

Resilience to environmental change

Risks and opportunities in our collective response

Introduction I am pleased to introduce the fourth edition of Risk Quarterly, our global publication offering timely insights into the fast-changing risk landscape. This issue brings together perspectives from Clyde & Co lawyers worldwide, alongside expert contributions from external voices, to explore the most pressing risks facing senior business leaders. Published to coincide with COP30 (10–21 November 2025, Belém, Brazil), this edition features multidisciplinary analysis on how climate change and ESG are reshaping governance, regulation, litigation, and insurance. Our lead article—by Dr Mark Bernhofen, Roberto Spacey Martín, and Professor Nicola Ranger of the Grantham Research Institute—examines the evolving regulatory landscape around environmental change. We explore how multinationals are responding to tariff turbulence by harnessing AI, restructuring supply chains, and rethinking business models. Additional topics include the legal risks of plastics, greenwashing litigation, the nuclear energy transition, and the surge in social inflation-related claims. We also examine emerging challenges around AI liability, copyright, and regulation. Finally, we share findings from the second part of our Corporate Risk Radar report, with market disruption of paramount concern, from new market entrants, technology and AI in the coming years. We hope you find this edition insightful and thought-provoking. Thank you to all contributors. If there are topics you’d like to see in future editions, please contact us at riskquarterly@clydeco.com.

Neil Beresford Partner

Scroll down

multiple global tipping thresholds (Armstrong McKay et al, 2022). A well-researched tipping point that reinforces the synergy between climate and nature is Amazon Forest dieback. Although the central estimate of the tipping threshold of this system is 3.5°C warming, deforestation amplifies these risks. Interactions between climate and deforestation could see the threshold passed at 20-25% deforestation, down from previous estimates of 40% (Lovejoy and Nobre, 2018), while impacts are estimated at USD 3.6 trillion (Lapola et al, 2018). However, other tipping points may materialise sooner with significant impact for finance. New research estimates USD 8 trillion of value at risk from water scarcity by 2050 for Global Systemically Important Banks alone, which would result in the collapse of some of these (Sabuco et al, forthcoming).

2024 marked not just another record-breaking year, but a fundamental shift in the velocity of change – global temperatures exceeded 1.5°C above pre-industrial levels for the first time over a 12-month period. We are approaching the Paris Agreement’s lower temperature threshold, which will result in more severe climate impacts. These impacts are already being felt today. Last year saw global losses of USD 320 billion from natural disasters (Figure 1), USD 140 billion of which were insured: the third most expensive year for the insurance industry since 1980 (Munich RE, 2025). These impacts extend beyond insurance, touching every corner of the global economy. Last summer, floods in central Europe shut down retailers and factories and disrupted critical infrastructure, impacting businesses not even directly affected by flooding (Reuters, 2024). Climate attribution analysis found that climate change made these floods twice as likely (Kimutai et al, 2024). In 2023, a record drought disrupted millions of tonnes of goods passing through the Panama Canal, with global supply chain impacts felt as far as Asia (IMF, 2023). Climate-related maritime trade impacts are estimated to exceed USD 80 billion annually (Verschuur et al, 2023). Climate risks are increasingly material business risks for all companies, regardless of location, because disruptions ripple through supply chains and

Current climate science and emerging physical risk trends

Key messages:

Compliance to competitve advantage

By Dr Mark Bernhofen, Roberto Spacey Martín, Professor Nicola Ranger

e are living in a period of accelerating environmental change. With this change comes risks and

W

opportunities. For businesses, the question is no longer whether to respond, but how. This article examines the evolving landscape of environmental resilience: from emerging physical risks to the shifting regulatory landscape, growth of resilience opportunities, and the evolving role of litigation, finance, and insurance. Organisations that take resilience seriously today will be best positioned to secure a competitive advantage as environmental risks intensify.

The risks from environmental change are becoming more apparent and businesses are increasingly feeling their effects.

Climate and nature risks interact and reinforce each other, raising concerns about passing critical tipping thresholds that could have substantial financial implications.

Data is vital and increasingly plentiful. Building capacity to interpret and use data is a strategic imperative.

shared infrastructure networks. As these risks intensify, organisations that prioritise climate preparedness will be better positioned to manage future challenges.

Beyond these observable climate impacts, two categories of emerging risk demand attention: the compound and cascading effect of climate change and nature loss, and the potential threat of earth system tipping points. Global nature and biodiversity loss are at an all-time high. Habitat destruction, overexploitation, and climate change are some of the drivers that have caused a 73% decline in wildlife populations since 1970 (WWF, 2024). The relationship between business and nature is one of double materiality; companies both contribute to environmental degradation and rely on the ecosystem services that nature provides. Take agriculture, for example. This sector is highly dependent on nature: 75% of all global flood crops rely on pollination, valued at hundreds of billions of dollars annually (Potts et al, 2010), while soil health and water

View Figure 1 here

regulation underpin all crop production. Nature loss also increases vulnerability to climate shocks, and the combined impacts of nature loss and climate change are macro-critical. Under compound climate and nature shock scenarios, the costs to the global economy could be upwards of USD 5 trillion (Ranger et al, 2023). The price impacts and resulting cascading risks should also not be underestimated. For example, recent empirical research shows that food price spikes can trigger food insecurity, public health risks, inflation, and political upheaval (Kotz et al, 2025).

Figure 1

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

Overall losses

Insured losses

0

100

200

300

400

Earth system tipping points may exponentially exacerbate these threats: the potential for sudden, cascading system failures that could reshape entire regions and sectors. Unlike gradual environmental change, tipping points represent thresholds where systems shift abruptly into new states that may be irreversible on human timescales. Tipping points exist for both climate and nature, and they can often interact and reinforce one another. Over 25 earth system tipping points have been identified using historical evidence and computer simulations (Lenton et al, 2023). We are nearing certain limits; global warming above the lower Paris Agreement limit of 1.5°C1 risks triggering

Model divergence is not inherently problematic; diversity in methodological approaches can illuminate uncertainty and reduce systemic risks (Heinrich et al, 2021). What is imperative is that organisations understand why models diverge and develop sufficient data literacy to integrate these data appropriately into decision-making. Initiatives such as the Climate Financial Risk Forum (CFRF) in the UK provide valuable guidance to support institutions in navigating the complexity of climate risk assessments. Recent guidance includes a scenario framework to assess risks and identify adaptation opportunities under uncertainty (CFRF, 2024)

Organisations cannot manage risks they do not measure. Effective risk management depends on robust data, and the landscape of available environmental data is expanding rapidly, with over 100 tools for assessing climate and nature risk detailed in UNEP FI’s latest Sustainability Risk Tool Dashboard (UNEP FI, 2025a). Yet this growth brings challenges: data divergence across providers, black-box methodologies, and limited quality oversight (Condon, 2023).

Policy & Regulatory Developments – Trajectories and Business Implications

Multilateral policy efforts are often slow but offset by relatively rapid deployment of domestic or regional policy whose impact can span across jurisdictions.

International, regional and domestic environmental policy has slowed down in 2025; however, industry trends continue to show signs of progress, and appetite remains for further action from business.

At COP30, Parties are expected to focus on three main areas: operationalising the Loss and Damage Fund; strengthening the Global Goal on Adaptation, including indicators for accountability; and advancing the fossil fuel transition agenda, last substantively addressed at COP28. Finance discussions will be anchored in the Baku-to-Belém Roadmap, which seeks to mobilise USD 300 billion annually by 2035 for climate action in developing countries, contributing to an overarching global target of USD 1.3 trillion mobilised by all actors (including the private sector). It is also hoped that parties submit updated National Adaptation Plans (NAPs), aligned with their revised NDCs, to better determine the adaptation finance gap, currently estimated at USD 387 billion/year until 2030 for developing countries alone (UNEP FI, 2024). However, submission of this too has been sluggish.

Attention is turning toward COP30 in Belém, Brazil, as the international community approaches a milestone moment: ten years since the Paris Agreement. One of the Agreement’s central enforcement mechanisms – states’ Nationally Determined Contributions (NDCs) - requires each Party to update its climate commitments every five years. Revised pledges made in 2020 narrowed the estimated temperature increase from around 4 °C to approximately 2.6–2.8 °C (UNEP FI, 2024). However, 2025 submissions have been more sluggish. As of 3rd October 2025, only 64 countries have submitted updated NDCs. Notable submissions include China’s commitment to reduce emissions 7–10% by 2035 from their peak, and the European Union’s indicative target of a 66–72 % reduction below 1990 levels. Collectively, these pledges indicate some progress but remain insufficient to align with the 1.5 °C trajectory (NZT, 2025; CAT, 2025). But it’s worth keeping in mind that trends outside of policy are promising – the International Energy Agency recently predicted that 50% of global electricity consumption for transport will come from renewables by 2030 (IEA 2025).

View Figure 2 here

+temperatures continue to rise after 2100

* If 2030 NDC targets are weaker than projected emissions

levels under policies & action, we use levels from policy & action

Policies & action

Real world action based on current policies +

Pledges & targets

Based on 2030 NDC targets* and

submitted and binding long-term targets

Optimistic scenario

Best case scenario and assumes full

implementation of all announced targets

including net zero targets, LTSs and NDCs*

CAT warming projections

Global temperature increase by 2100

November 2024 update

+4°C

+3°C

+2°C

+1.5°C

+0°C

Global mean

temperature

increase by

2100

+3.4°C

+2.7°C

Policies

& action

+2.2°C

+3.2°C

+2.6°C

2030

targets

only

1.5°C PARIS AGREEMENT GOAL

WE ARE HERE

1.3°C WARMING IN 2023

+2.1°C

Pledges &

+1.7°C

+2.4°C

+1.9°C

Optimistic

scenario

PRE-INDUSTRIAL AVERAGE

Figure 2

2030 targets only

Based on 2030 NDC targets* +

Figure 1. Natural disasters losses (and insured losses) worldwide 1980-2024. Source: Munich Re, 2025.

The International Court of Justice’s (ICJ) advisory opinion on climate change, delivered in July 2025, has added further momentum to climate governance this year and raised hopes for some (e.g. LSE, 2025). The Court provided an expansive interpretation of states’ obligations under international law, which, though non-binding, is expected to inform policy development, judicial reasoning, and corporate due diligence expectations.

Alongside the multilateral climate negotiations, the Kunming–Montreal Global Biodiversity Framework continues to inform international action and national regulation on nature. 55 countries have now developed National Biodiversity Strategy and Action Plans (the nature-equivalent of NDCs) with over 3,300 national targets set (CBD 2025). These trends at the international stage are likely to guide the domestic and regional policy developments that shape the operating environment for business.

In the regulatory sphere, developments now span financial, sectoral, fiscal, and environmental instruments. Disclosure standards remain a core pillar. The International Sustainability Standards Board (ISSB)’s IFRS S1 and S2 have been adopted or are under consideration in more

than 36 jurisdictions (IFRS, 2025), while the Transition Plan Taskforce (TPT) recommendations are increasingly referenced by regulators and investors (e.g. Australia’s Treasury (2025), the European Banking Authority (2025) and the Hong Kong Monetary Authority (2024)). Beyond disclosure, governments are deploying complementary tools:

Fiscal measures, such as carbon pricing, tax credits, and green procurement, are steering capital flows. More than 70 national or subnational carbon pricing initiatives are now in operation or development (World Bank, 2025).

Sector-specific regulation is expanding, from the Carbon Border Adjustment Mechanism (CBAM) to mandatory climate-resilient water resource planning in England and national energy-efficiency standards for buildings and transport in several jurisdictions (Environment Agency, 2024).

Market-based mechanisms are evolving, including the consolidation of voluntary carbon markets under new integrity frameworks (e.g. the Carbon Offsetting and Reduction Scheme for International Aviation) and regional emissions-trading schemes being refined in Asia and Latin America, under Article 6 of the Paris Agreement.

Public finance and blended-capital models are increasingly being used to address adaptation and resilience gaps, creating new opportunities for insurers, lenders, and infrastructure investors (Convergence, 2024).

For corporates, these developments signal a growing overlap between climate, nature, and financial regulation. The slow but steady progress of multilateral agreements at the international level is complemented by often comparatively rapid development of domestic regulation, whose impact can span across sectors and value chains. 2025 has witnessed a change of pace across the board, as suitable regulation is being reflected on, consolidated and reappraised in light of other policy priorities. However, recent data shows that 98% of companies find climate change to be a material topic for disclosure (EFRAG 2025). This trend is echoed by the financial sector’s growing appetite for non-financial information disclosure and performance (PWC, 2024; Larcker et al, 2024; Krueger et al, 2024; IOSCO, 2024). Despite some slowdown, the overarching march of regulation coupled with growing industry trends, and the evolving risk landscape are therefore incentivising companies to act on climate- and other nature-related risks and opportunities.

The economic rationale for adaptation and resilience investments

Investment in resilience has been demonstrated to provide a triple dividend of benefits.

Financing opportunities for adaptation and resilience are expected to improve given the underlying economics and emerging financial innovation.

As providers of goods, services, employment and investment, the private sector plays a crucial role in building resilience to environmental change. In adapting to environmental change, firms can secure wider resilience benefits for society by generating resilience services, jobs and growth, while failing to adapt effectively can also harm our collective resilience. Investment into resilience is therefore argued to deliver three types of benefits: avoiding losses from acute or chronic risks; generating economic benefits by stimulating economic activity; and strengthening social and natural capital for wider social and environmental benefits (Surminski and Tanner, 2016; GCA, 2019; Heubaum et al, 2022). The latter two are particularly important as they materialise even without a risk event occurring. A recent quantitative analysis of these benefits has found that every USD 1 invested into adaptation can yield USD 10.53 over a 10-year time period with average returns of 27% (Brandon et al, 2025).

Recent developments in tools used to assess the risks and opportunities emerging from environmental change equip corporates to pursue adaptation and resilience opportunities. Influential platforms such as the Network for Greening the Financial System (NGFS) and the UK Climate Financial Risk Forum (CFRF) have driven effective use of scenarios in forward-looking risk assessments for regulators, financial institutions and corporates (NGFS 2025, CFRF 2024). Other frameworks have begun to integrate nature-related risks into these assessments (Ranger et al 2023, Ranger et al 2024), enhancing understanding of the specific ways in which the links between climate, nature and society serve as sources of risk and opportunity. Targeting corporates in particular, the Physical Climate Risk Appraisal Methodology (PCRAM) provides authoritative guidelines for integrating climate-related physical risk into investment decision-making and understanding how adaptation actions can modulate asset value losses (IIGCC, 2025). Further guidance for corporates has also been issued on how adaptation and resilience can be integrated into transition plans and broader business planning (CFRF 2024, WBCSD 2025, UNEP FI 2025b). Together, these frameworks and methodologies have equipped corporates with the tools to make economic and rational cases for taking action in response to climate change.

At the same time, financing opportunities are also likely to improve for adaptation and resilience due to the underlying economic rationale. Exposure to climate-related physical risk has been empirically shown to affect credit ratings (Capiello et al, 2025), and as a result, modelled adaptation actions can have positive effects on credit ratings (Bernhofen et al, 2024). Although corporate disclosure on adaptation and resilience is limited (Spacey Martín et al, 2025), research has shown that even the current limited volume of information is vastly under-utilised for sustainability-linked finance (Resendiz et al, 2025a). Similar empirical results have been found in relation to nature (Resendiz et al, 2025b). These trends, together with further innovations in risk transfer, liquidity arrangements and other areas, are poised to strengthen the economic benefits for firms and financial institutions taking action on adaptation and resilience.

The evolving role of litigation, finance, and insurance

Climate litigation is no longer just about emissions; it’s increasingly targeting inadequate preparedness for physical climate impacts.

Adaptation and nature financing gaps represent not just a funding challenge, but a major market opportunity that sophisticated investors are beginning to capture.

Rising climate risks are putting the insurance industry under increasing strain. Its role in absorbing residual risk remains vital, but the sector can also incentivize adaptation through risk-based pricing and cross-industry partnerships.

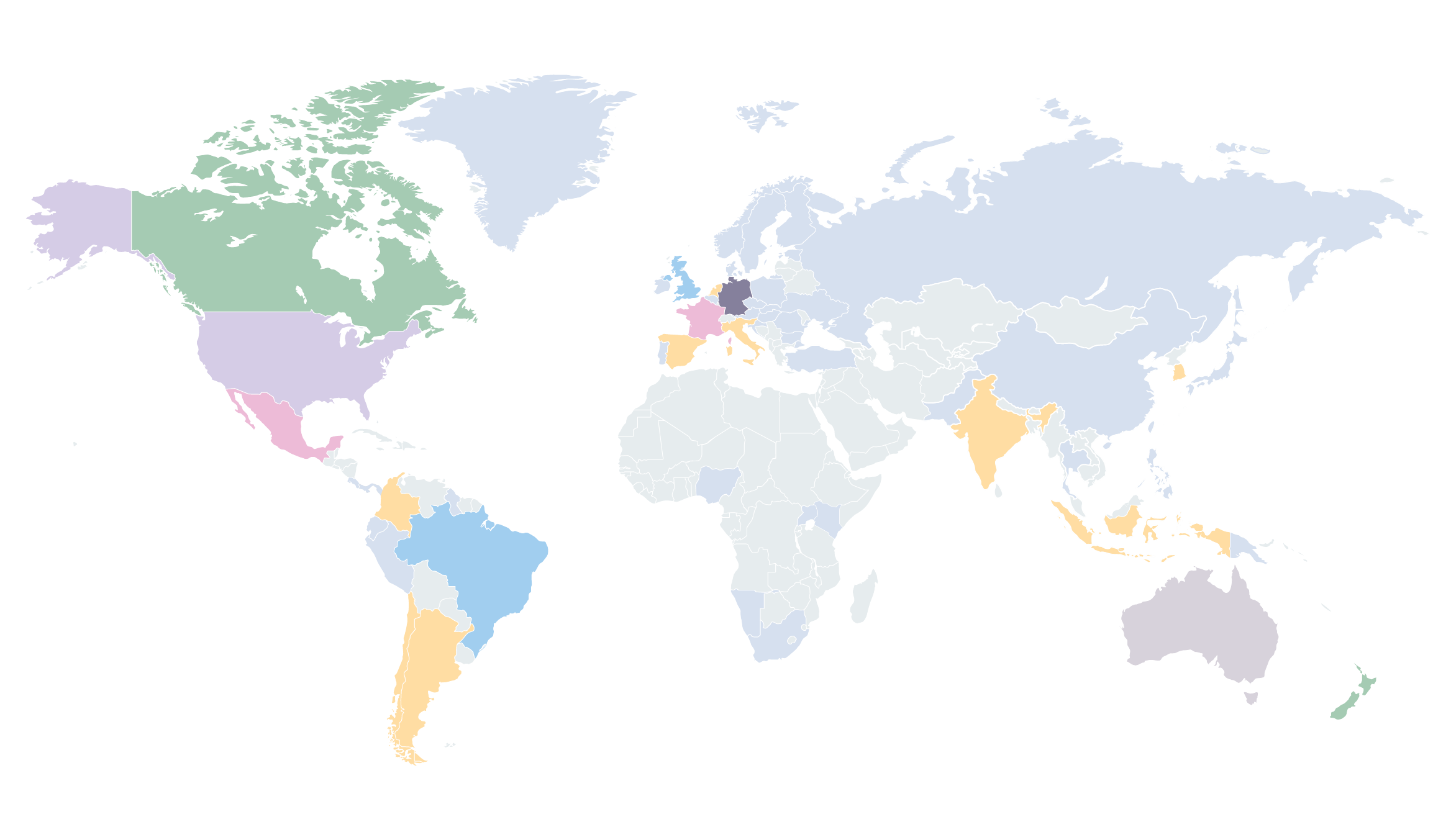

Litigation Over the last decade, climate litigation has grown in importance and now plays an increasingly central role in combating the climate crisis. By the end of 2024, the number of climate litigation cases globally (see Figure 3) reached nearly 3,000 (Setzer and Higham, 2025). Climate litigation has evolved from challenges to administrative procedures in the US and Australia in the 1980s to a global effort to hold governments and private actors to account for climate inaction today (Bradeen, 2024). Recent growth in litigation cases has been catalysed by the signing of the Paris Agreement in 2015 as well as recent advances in attribution science, which can establish the causal link between a country or corporation’s historic emissions and climate impacts (Stuart-Smith et al, 2021). In July 2025, this trajectory of expanding legal accountability reached the highest level of international law when the ICJ issued its landmark statement on the obligation of states with respect to climate.

View Figure 3 here

While the ICJ opinion (discussed in the previous section) addressed states’ obligations, it has significant implications for businesses (see Lawrence and Williams, 2025). The Court confirmed states must regulate private actors under their jurisdiction, particularly regarding fossil fuel activities and emissions, while affirming the IPCC as the “best available science” and that emissions can be legally attributed to specific actors. Financial markets are already pricing these risks (Sato et al, 2024). Research surveying 800 investors found that 80% consider climate litigation at least moderately important to firm value, and 41% believe it already affects financial performance (Gostlow et al, forthcoming, cited in CETEX, 2025).

Companies are also facing growing litigation for inadequate adaptation (Setzer and Higham, 2025). Legal action can either occur before any physical impacts, such as for inadequate disclosure or for failing to comply with adaptation regulation, or it can come after a physical impact, for failing to mitigate the risks that have been incurred (UNEP FI, 2021).

For businesses, the message is unambiguous: climate litigation will continue to accelerate in scope and sophistication, making climate risk management and credible action strategic necessities rather than voluntary commitments.

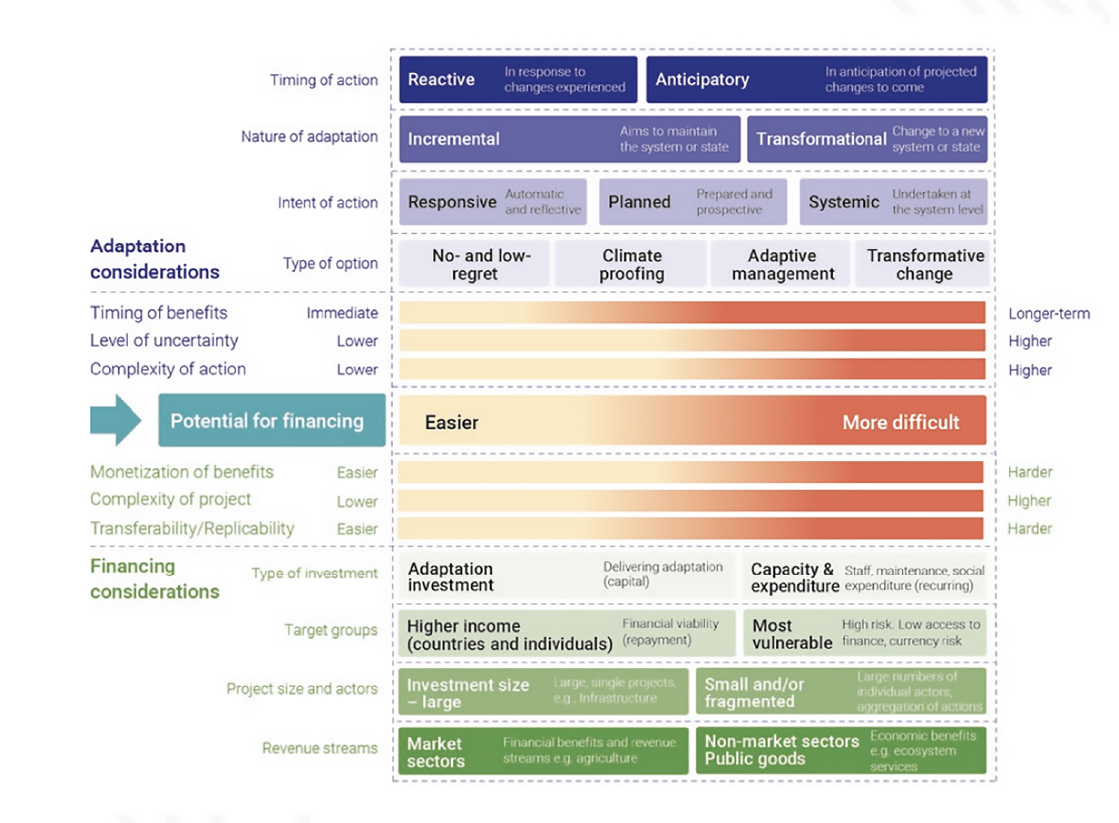

Finance Despite the compelling economic case for resilience, public finance continues to flow at a fraction of what is needed. Current annual financing gaps until 2030 stand at USD 387 billion for adaptation in EMDEs (UNEP FI, 2024) and USD 700 billion for biodiversity globally (Convention on Biological Diversity, 2022). Notwithstanding the suitability constraints of private finance to secure adaptation and resilience benefits (see Figure 4), there is a need for private finance to step up. The challenge will not be solved only by mobilising new types of finance for adaptation, resilience and nature. Existing financial flows must also be aligned with resilience and nature, as part of sound management of uncertain yet systemic risks. This means that institutions must move beyond defensive risk management to actively building resilience in the systems and societies in which they operate (Mullan and Ranger 2022).

View Figure 4 here

Figure 4

Figure 4. Types of adaptation actions and associated financing considerations. Source: UNEP Adaptation Gap Report 2024.

Portfolio management of climate- and nature-related risk, coupled with the strengthening economic rationale for adaptation and resilience investment, has translated into tangible investor interest. Multiple investment frameworks have been published to guide investors seeking portfolio exposure to resilience opportunities (Standard Chartered 2024, Goldman Sachs 2023, BlackRock 2023). Adaptation and resilience are also being introduced into sustainable investment taxonomies at the jurisdictional level (Spacey Martín et al, 2024). The London Stock Exchange Group (2025) recently estimated that USD 1 trillion in corporate revenue is derived from adaptation and resilience activities, with a compound annual growth rate of 5% since 2016. These trends are reflective of a financial sector increasingly hungry to enter the adaptation and resilience market, representing a significant opportunity for corporates. New innovative financing instruments are emerging (e.g. adaptation-smart credit ratings, sustainability-linked financing), and support from government (i.e. through blended financing) is pushing frontiers on investability.

Insurance Insurance is a critical enabler of resilience – both directly and indirectly. Not all risks can be adapted away, and insurance can play an important role in absorbing the residual risks and supporting governments, households and businesses in recovering from disasters. In speeding recovery, insurance can reduce the overall costs of disasters. It also provides an important risk signal – risk-based pricing can create rewards for resilience, catalysing adaptation investment.

The reframing of environmental change from a risk to an opportunity has the potential to unlock capital at scale, creating a powerful tailwind for companies that can demonstrate not just adaptation plans but investible resilience solutions.

However, as climate change increases risk exposure, the insurance sector faces growing challenges. Demand could grow as risks rise, but rising risks can also make insurance unaffordable. At the same time, greater uncertainty in risk or pricing pressures from government can make it more difficult for insurers to offer coverage. Examples include the withdrawal of some major insurers from California’s wildfire-exposed market. In response, the insurance industry is innovating rapidly. Parametric insurance products, which pay out based on predefined triggers (such as wind speed or rainfall levels) rather than assessed losses, are gaining traction due to their rapid payouts, reduced administrative costs, and ability to cover risks that are difficult to insure through traditional models. The parametric insurance market is projected to grow from US$18 billion in 2023 to US$34.4 billion by 2033, driven by increasing climate losses and the development of new technologies that enable these products (Allied Market Research, 2024).

USD 18 billion in 2023 to USD 34.4 billion by 2033, driven by increasing climate losses and the development of new technologies that enable these products (Allied Market Research, 2024).

Beyond risk transfer, the insurance industry may choose to do more to catalyse resilience through pricing mechanisms that reward adaptation investments (OECD, 2023). For example, in the US, some insurance companies offer discounts to homes that meet hurricane-resilient building standards. A study following Hurricane Sally in Alabama found that the hurricane-resilient homes reduced the frequency of claims by up to 74% (Alabama Department of Insurance, 2025). The sector can also extend its impact on adaptation and resilience through initiatives such as the Insurance Development Forum (IDF), which is a public-private partnership that supports the use of insurance and risk modelling to support resilience and close the protection gap in emerging and developing economies. The IDF’s footprint is in 30 countries, it has built technical capacity through training programs for over 100 supervisors, invested USD 900,000 in open-access risk data, and co-financed USD 30 million in disaster risk financing mechanisms in EMDEs (Mahoul and Ranger, 2024).

Environmental change is accelerating, and the distinction between leaders and laggards will increasingly hinge on preparedness. Organisations that integrate climate and nature risks into strategy, build robust data capabilities, and pursue resilience as a competitive advantage will be best positioned for long-term success. The regulatory trajectory is clear despite recent slowdowns, and the economic case for adaptation is strengthening. The question is no longer whether to act, but how quickly and strategically organisations can transform risk into opportunity.

CONCLUSION

Bibliography

Alabama Department of Insurance & Center for Risk and Insurance Research. (2025, May 5). Performance of IBHS FORTIFIED Home Construction in Hurricane Sally. University of Alabama. https://www.aldoi.gov/pdf/news/performanceibhsfortifiedhomeconstructionhurricanesally.pdf Allied Market Research. (2024). Parametric Insurance Market Size, Share, Competitive Landscape and Trend Analysis Report, by Type (Natural Catastrophes Insurance, Specialty Insurance, Others), by Industry Vertical (Agriculture, Aerospace and Defense, Mining, Construction, Energy and Utilities, Manufacturing, Others): Global Opportunity Analysis and Industry Forecast, 2023–2033. Allied Market Research. https://www.alliedmarketresearch.com/parametric-insurance-market-A14966 Alvarez, J., et al. (2025). Evidence review on the financial effects of nature-related risks. TNFD Discussion Papers. https://tnfd.global/publication/evidence-financial-effects-of-nature-related-risks/ Armstrong McKay, D. I., et al. (2022). Exceeding 1.5 °C global warming could trigger multiple climate tipping points. Science. https://www.science.org/doi/10.1126/science.abn7950 Australian Government. (2025, August). Climate-related Transition Planning Guidance: Consultation Paper. Australian Government. https://consult.treasury.gov.au/c2025-683229 Bernhofen, M., et al. (2024). The Impact of Physical Climate Risks and Adaptation on Sovereign Credit Ratings. SSRN. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4950708 BlackRock. (2023). Climate resilience: An emerging investment theme. BlackRock Investment Institute. https://welectric.pt/wp-content/uploads/2023/12/bii-megaforces-december-2023.pdf Bradeen, E. (2024). What is climate litigation? Grantham Research Institute on Climate Change and the Environment, London School of Economics and Political Science. https://www.lse.ac.uk/granthaminstitute/explainers/what-is-climate-change-litigation/ Brandon, C., et al. (2025). Strengthening the investment case for climate adaptation: A triple dividend approach. World Resources Institute. https://files.wri.org/d8/s3fs-public/2025-06/strengthening-investment-case-climate-adaptation.pdf?VersionId=een52ahEiIO4IaOA6e8ps4fQCN4xTtph Capiello, L., et al. (2025). From words to deeds – Incorporating climate risks into sovereign credit ratings. European Central Bank. https://www.ecb.europa.eu/press/research-publications/resbull/2025/html/ecb.rb250730~ebfb33d43c.en.html CETEX. (2025). Submission to the UK Government consultation ‘Climate-related transition plan requirements’. Centre for Economic Transition Expertise, TPI Global Climate Transition Centre, and Grantham Research Institute, London School of Economics and Political Science. https://cetex.org/publications/submission-to-the-uk-government-consultation-climate-related-transition-plan-requirements/ CFRF. (2024). Mobilizing adaptation finance to build resilience. Climate Financial Risk Forum Adaptation Working Group. https://www.fca.org.uk/publication/corporate/cfrf-mobilising-adaptation-finance-build-resilience-2024.pdf Climate Action Tracker [CAT]. (2025). Mid-year check on 2035 climate plans. Climate Action Tracker. https://climateactiontracker.org/publications/mid-year-check-on-2035-climate-plans/ Condon, M. (2023). Climate services: The business of physical risk. Arizona State Law Journal. https://arizonastatelawjournal.org/2023/08/01/climate-services-the-business-of-physical-risk/ Convention on Biological Diversity. (2022). Kunming–Montreal Global Biodiversity Framework. CBD Secretariat. https://www.cbd.int/gbf Convention on Biological Diversity. (2025). Online reporting tool. CBD Secretariat. https://ort.cbd.int/?_gl=1*v2amiq*_ga*MTE5ODkyNjg3Mi4xNzU5NjA3NDgz*_ga_7S1TPRE7F5*czE3NTk5MzY4NDckbzMkZzAkdDE3NTk5MzY4NDckajYwJGwwJGgw#0.4/0/0

MEET THE AUTHORS

Professor Nicola Ranger Executive Director, Earth Capital Nexus, and Professor in Practice of Natural Capital, Risk and Finance, The London School of Economics and Political Science

Roberto Spacey Martín Resilience Alignment Lead, Earth Capital Nexus, The London School of Economics and Political Science

Dr. Mark Bernhofen Post-Doctoral Researcher, University of Oxford and The London School of Economics and Political Science

Mark is a post-doctoral academic researcher working at the University of Oxford and the London School of Economics. His research focuses on climate risk and adaptation, with a particular emphasis on the use of climate risk data for decision-making. Mark’s work spans multiple sectors: modelling physical climate risk impacts on sovereign credit ratings, developing asset and firm-level climate financial risk methodologies for financial institutions, and creating climate risk assessment approaches to support humanitarian organisations.

Roberto Spacey Martín is a researcher focused on aligning financial systems with the resilience of ecosystems and societies. As Resilience Alignment Lead within HYPERLINK “https://www.lse.ac.uk/granthaminstitute/ecn/”Earth Capital Nexus at the London School of Economics and Political Science, he develops evidence-based tools and metrics to integrate climate and nature into financial decision-making. His research explores the use of resilience and nature-alignment metrics in transition plans, industry benchmarks, investment decision-making, financial policy, and regulatory supervision.

Professor Nicola Ranger is Executive Director of Earth Capital Nexus and Professor in Practice of Natural Capital, Risk and Finance in the Grantham Research Institute on Climate Change and the Environment at the London School of Economics and Political Science. She is a global expert and leads interdisciplinary research and policy engagement at the nexus of finance, investment, natural capital, resilience and sustainable development with a global focus.

Click photos to find out more

Figure 3

1-10

11-20

21-30

31-40

60-70

130-149

150-170

1,890-1,900

None

Jordan

Oman

Chile

Argentina

Paraguay

French

Guiana

Brazil

Bolivia

Portugal

Norway

Belgium

Sweden

Turkiye

Ireland

Iraq

Iran

Kazakhstan

Turkmenistan

Yemen

Saudi Arabia

Egypt

Libya

Niger

Mali

Ghana

Syria

Peru

Canada

Finland

Poland

Ukraine

Greenland

Russia

China

Japan

South Africa

Sudan

Madagascar

Zimbabwe

Zambia

Mozambique

Kenya

Tanzania

Somalia

Ethiopia

Uganda

Namibia

Angola

Gabon

Cameroon

Liberia

Morocco

Algeria

Western

Sahara

Mauritania

Senegal

Guinea

Congo

New Zealand

Papua New

Philippines

Malaysia

Vietnam

Thailand

India

Bangladesh

Nepal

Myanmar

Uzbekistan

Pakistan

Australia

United States

Monaco

Mexico

France

Italy

Colombia

Uruguay

Dr Congo

Chad

Sierra Leone

Nigeria

Romania

UAE

Spain

Hungary

Czechia

United

Kingdom

Netherland

Estonia

Azerbaijan

Afghanistan

Botswana

Suriname

Latvia

Lithuania

Belarus

Mongolia

North Korea

Venezuela

Haiti

Belize

Cuba

Dominican

Republic

Panama

Honduras

Guatemala

Nicaragua

Costa Rica

Guyana

Ecuador

Indonesia

Austria

Germany

South Korea

Read more >>

Convergence. (2024). State of blended finance 2024: Climate edition. Convergence. https://ppp.worldbank.org/sites/default/files/2025-06/State%20of%20Blended%20Finance%202024-%20Climate%20Edition.pdf Environment Agency. (2024). A summary of England’s revised draft regional water resources management plans. Environment Agency. https://www.gov.uk/government/publications/a-review-of-englands-draft-regional-and-water-resources-management-plans/a-summary-of-englands-draft-regional-and-water-resources-management-plans European Banking Authority [EBA]. (2025). Final Report on Guidelines on the Management of Environmental, Social and Governance (ESG) Risks (EBA/GL/2025/01). EBA. https://www.eba.europa.eu/sites/default/files/2025-01/fb22982a-d69d-42cc-9d62-1023497ad58a/Final%20Guidelines%20on%20the%20management%20of%20ESG%20risks.pdf European Financial Reporting Advisory Group [EFRAG]. (2025). EFRAG 2025 State of Play. EFRAG. https://insights.efrag.org/dashboard Global Commission on Adaptation [GCA]. (2019). Adapt now: A global call for leadership on climate resilience. Global Commission on Adaptation. https://gca.org/reports/adapt-now-a-global-call-for-leadership-on-climate-resilience/ Goldman Sachs. (2025). GS SUSTAIN: Adaptation, Mitigation, Physical Risk – Where We Expect to See Investment Tailwinds and Why. Goldman Sachs Research. https://www.goldmansachs.com/insights/goldman-sachs-research/where-we-expect-to-see-investment-tailwinds-and-why Heinrich, Y., et al. (2022). A simulation of the insurance industry: The problem of risk model homogeneity. Journal of Economic Interaction and Coordination. https://link.springer.com/article/10.1007/s11403-021-00319-4 Heubaum, H., et al. (2022). The triple dividend of building climate resilience: Taking stock, moving forward. World Resources Institute. https://files.wri.org/d8/s3fs-public/2022-11/triple-dividend-climate-finance.pdf?VersionId=eWpTL9Q41jtpDXqg98FFdF6x8V.Fyqo1 Hong Kong Monetary Authority [HKMA]. (2024). Annex: Good practices on transition planning. HKMA. https://brdr.hkma.gov.hk/eng/doc-ldg/docId/20241218-2-EN Hughes, T. P., et al. (2017). Coral reefs in the Anthropocene. Nature. https://www.nature.com/articles/nature22901 IFRS. (2025). IFRS Foundation publishes jurisdictional profiles providing transparency and evidencing progress towards adoption of ISSB Standards. IFRS. https://www.ifrs.org/news-and-events/news/2025/06/ifrs-foundation-publishes-jurisdictional-profiles-issb-standards/ International Court of Justice. (2025, July 23). Obligations of States in Respect of Climate Change: Advisory Opinion. ICJ. https://www.icj-cij.org/case/187 International Energy Agency [IEA]. (2025). Renewables 2025. IEA. https://www.iea.org/reports/renewables-2025 Institutional Investors Group on Climate Change [IIGCC]. (2025). Physical Climate Risk Appraisal Methodology (PCRAM) 2.0. IIGCC. https://www.iigcc.org/resources/consultation-physical-climate-risk-appraisal-methodology-2.0 International Monetary Fund [IMF]. (2023). Climate change is disrupting global trade. IMF. https://www.imf.org/en/Blogs/Articles/2023/11/15/climate-change-is-disrupting-global-trade International Organization of Securities Commissions [IOSCO]. (2024). IOSCO Report on Transition Plans. IOSCO. https://www.iosco.org/library/pubdocs/pdf/IOSCOPD772.pdf

Kimutai, J., et al. (2024). Climate change and high exposure increased costs and disruption to lives and livelihoods from flooding associated with exceptionally heavy rainfall in Central Europe. World Weather Attribution. https://www.worldweatherattribution.org/climate-change-and-high-exposure-increased-costs-and-disruption-to-lives-and-livelihoods-from-flooding-associated-with-exceptionally-heavy-rainfall-in-central-europe/ Kotz, M., et al. (2025). Climate extremes, food price spikes, and their wider societal risks. Environmental Research Letters. https://iopscience.iop.org/article/10.1088/1748-9326/ade45f Krueger, P., et al. (2024). The effects of mandatory ESG disclosure around the world. Journal of Accounting Research. https://onlinelibrary.wiley.com/doi/10.1111/1475-679X.12548 Lapola, D. M., et al. (2018). Limiting the high impacts of Amazon forest dieback with no-regrets science and policy action. PNAS. https://www.pnas.org/doi/10.1073/pnas.1721770115 Larcker, D. F., et al. (2024). 2024 Institutional Investor Survey on Sustainability. Stanford University, CGRI Survey Series. https://www.gsb.stanford.edu/faculty-research/publications/2024-institutional-investor-survey-sustainability Lawrence, W., & Williams, L. (2025). The development of international law on climate change. Clyde & Co Insights. https://www.clydeco.com/en/insights/2025/09/the-development-of-international-law-on-climate-ch Lenton, T., et al. (2023). The Global Tipping Points Report. University of Exeter. https://report-2023.global-tipping-points.org/?_gl=1%2A1t9x2qo%2A_gcl_au%2ANDIzNjI0MDc1LjE3NTk4MzI3NDY.%2A_ga%2AMTk1NjI2MzUwNS4xNzU5ODMyNzQ2%2A_ga_D45K1N753J%2AczE3NTk4MzI3NDUkbzEkZzEkdDE3NTk4MzM0NzkkajYwJGwwJGgw Lovejoy, T. E., & Nobre, C. (2018). Amazon tipping point. Science Advances. https://www.science.org/doi/full/10.1126/sciadv.aat2340 London School of Economics [LSE]. (2025). Institute responds to International Court of Justice advisory opinion. LSE Press Release. https://www.lse.ac.uk/granthaminstitute/news/institute-responds-to-international-court-of-justice-advisory-opinion/ London Stock Exchange Group [LSEG]. (2025). Investing in the green economy 2025: Navigating volatility and disruption. LSEG. https://www.lseg.com/content/dam/lseg/en_us/documents/sustainability/investing-in-green-economy-2025.pdf Mahoul, O., & Ranger, N. (2024). How insurance fuels action for development, climate and biodiversity goals. Oxford Martin School. https://www.oxfordmartin.ox.ac.uk/blog/how-insurance-fuels-action-for-development-climate-and-biodiversity-goals Mullen, M., & Ranger, N. (2022). Climate-resilient finance and investment: Framing paper. OECD. https://www.oecd.org/en/publications/climate-resilient-finance-and-investment_223ad3b9-en.html Munich Re. (2025). Climate change is showing its claws: The world is getting hotter, resulting in severe hurricanes, thunderstorms and floods. Munich Re. https://www.munichre.com/en/company/media-relations/media-information-and-corporate-news/media-information/2025/natural-disaster-figures-2024.html#-1537950557 Net Zero Tracker [NZT]. (2025). Net Zero Stocktake 2025. Net Zero Tracker. https://zerotracker.net/analysis/net-zero-stocktake-2025 Network for Greening the Financial System [NGFS]. (2025). NGFS Scenarios Portal. NGFS. https://www.ngfs.net/ngfs-scenarios-portal/ Organisation for Economic Co-operation and Development [OECD]. (2023). Enhancing the insurance sector’s contribution to climate adaptation. OECD. https://www.oecd.org/en/publications/enhancing-the-insurance-sector-s-contribution-to-climate-adaptation_0951dfcd-en.html

otts, S. G., et al. (2010). Global pollinator declines: Trends, impacts and drivers. Trends in Ecology & Evolution. https://www.cell.com/trends/ecology-evolution/fulltext/S0169-5347(10)00036-4?cc=y PricewaterhouseCoopers [PWC]. (2024). PwC’s Global Investor Survey 2024. PwC. https://www.pwc.com/gx/en/issues/c-suite-insights/global-investor-survey.html Ranger, N., et al. (2023). The Green Scorpion: The macro-criticality of nature for finance – Foundations for scenario-based analysis of complex and cascading physical nature-related risks. University of Oxford. https://www.ngfs.net/system/files/import/ngfs/medias/documents/ngfs_occasional_paper_green-scorpion_macrocriticality_nature_for_finance.pdf Ranger, N., et al. (2024). Toward greening finance for nature: Assessing the materiality of nature-related financial risk for the UK. Green Finance Institute. https://www.greenfinanceinstitute.com/wp-content/uploads/2024/06/GFI-GREENING-FINANCE-FOR-NATURE-FINAL-FULL-REPORT-RDS4.pdf Resendiz, J. L., et al. (2025a). Sustainability-linked finance: A lever for firm-level resilience innovation. Grantham Research Institute. https://www.lse.ac.uk/granthaminstitute/wp-content/uploads/2025/09/working-paper-429-Resendiz-et-al.pdf Resendiz, J. L., et al. (2025b). Sustainability-linked finance: Bridging nature disclosure gaps in Southeast Asia. Grantham Research Institute. https://www.lse.ac.uk/granthaminstitute/wp-content/uploads/2025/06/working-paper-427-Resendiz-et-al.pdf Reuters. (2024). Central Europe factories and retailers shut in flood-hit areas. Reuters. https://www.reuters.com/world/europe/central-europe-factories-retailers-shut-flood-hit-areas-2024-09-16/ Sadler, A., et al. (2024). The impact of COVID-19 fiscal spending on climate change adaptation and resilience. Nature Sustainability. https://www.nature.com/articles/s41893-024-01269-y Setzer, J., & Higham, C. (2025). Global Trends in Climate Change Litigation: 2025 Snapshot. Grantham Research Institute, London School of Economics and Political Science. https://www.lse.ac.uk/granthaminstitute/publication/global-trends-in-climate-change-litigation-2025-snapshot/ Smoleńska, A., et al. (2025). Banks and climate litigation risk: Navigating the low carbon transition. London School of Economics and Political Science. https://cetex.org/publications/banks-and-climate-litigation-risk-navigating-the-low-carbon-transition/ Spacey Martín, R., et al. (2024). The (in)coherence of adaptation taxonomies. SSRN. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4874598 Spacey Martín, R., et al. (2025). Empirically assessing corporate adaptation and resilience disclosures using AI. Grantham Research Institute. https://www.lse.ac.uk/granthaminstitute/wp-content/uploads/2025/09/working-paper-430-Spacey-Martin-et-al.pdf Standard Chartered. (2024). Guide for Adaptation and Resilience Finance. Standard Chartered. https://www.sc.com/en/adaptation-resilience-finance-guide/ Stuart-Smith, R., et al. (2021). Attribution science and litigation: Facilitating effective legal arguments and strategies to manage climate emissions. FILE Foundation. https://www.smithschool.ox.ac.uk/sites/default/files/2022-03/attribution-science-and-litigation.pdf Surminski, S., & Tanner, T. (2016). Realising the “Triple Dividend of Resilience”: A new business case for disaster risk management. Springer. https://link.springer.com/book/10.1007/978-3-319-40694-7

Verschuur, J., et al. (2023). Systemic risks from climate-related disruptions at ports. Nature Climate Change. https://www.nature.com/articles/s41558-023-01754-w United Nations Environment Programme [UNEP]. (2024). Emissions Gap Report 2024. UNEP. https://lsecloud-my.sharepoint.com/personal/r_spacey-martin_lse_ac_uk/Documents/-%20https:/www.unep.org/resources/emissions-gap-report-2024 United Nations Environment Programme Finance Initiative [UNEP FI]. (2021). Liability risk and adaptation finance. UNEP FI. https://www.unepfi.org/themes/climate-change/liability-risk-and-adaptation-finance/ United Nations Environment Programme Finance Initiative [UNEP FI]. (2024). Adaptation Gap Report 2024. UNEP FI. https://www.unep.org/resources/adaptation-gap-report-2024 United Nations Environment Programme Finance Initiative [UNEP FI]. (2025a). Database: Sustainability Risk Tool Dashboard. UNEP FI. https://www.unepfi.org/themes/climate-change/the-sustainability-risk-tool-dashboard/ United Nations Environment Programme Finance Initiative [UNEP FI]. (2025b). Practical Guidance on Implementing Adaptation and Resilience for Banks. UNEP FI. https://www.unepfi.org/industries/banking/adaptation-resilience-guidance/ World Business Council for Sustainable Development [WBCSD]. (2025). Adaptation planning for business: Navigating uncertainty to build long-term resilience. WBCSD. https://www.wbcsd.org/resources/adaptation-planning-for-business-navigating-uncertainty-to-build-long-term-resilience/?submitted=true World Wide Fund for Nature [WWF]. (2024). Living Planet Report 2024 – A system in peril. WWF.

<< Back page

Figure 2. Global temperature trajectories by 2100 under different policy scenarios. Figure reflects policies up to November 2024.

Figure 3. Number of climate litigation cases filed in national courts, globally (to end of 2024). Source: Setzer and Higham, 2025.

References: The Paris Agreement, adopted by 195 countries in 2015, is a treaty that aims to limit global temperature increase to well below 2°C, with efforts to limit warming to 1.5°C. Global warming levels are calculated relative to a pre-industrial (1850-1900) climate and averaged over a period of at least 20 years.

What’s the state of play for multinationals today?

ESG in 2025:

Stakeholder impetus remains strong

Mitigating risk and building resilience

In Asia, recent moves by countries including China, Japan and Singapore to implement the sustainability disclosure standards set out by the International Sustainability Standards Board (ISSB) highlight a desire among many regional administrations to raise the bar on ESG.4 Meanwhile, in the Middle East, 2025 has seen both the UAE5 and Jordan6 launch mandatory climate reporting frameworks.

ESG still very much matters in 2025 but it is evolving rapidly and presenting multinationals with new challenges. This is reflected in our latest Corporate Risk Radar research findings, which reveal that more CEOs, board members and General Counsel in 2025 rated climate change and societal risks as “high-impact” than in 2024 (rising to 44% from 31%, and 29% from 23%, respectively).10 In the current climate, companies with global operations and supply chains must not only comply with divergent and changeable sets of regulations. They may also need to reassess whether their risk frameworks remain fit for purpose, while rethinking how to demonstrate the value of their ESG activities and maintain consistency of messaging across the board. All while being alert to the heightened sensitivities that exist among different stakeholder groups around the world. It’s a fine line to tread.

Rethinking ESG?

Importantly for multinationals, the changes seek to create consistency across the EU by aligning the rules with other legislation and preventing member states from imposing stricter rules on a national basis. However, concerns have emerged in some quarters over the uncertainty that could be created, and the potential for non-EU companies to come within scope of the rules.

In the US, federal regulations requiring companies to report on the environmental impact of their operations and their climate-related risk mitigation activities (under the SEC’s Climate Disclosure Rules) have been cancelled.1 That doesn’t mean, however, that businesses will necessarily be exempt from reporting requirements, since states such as California2 (not to mention many other countries around the world) are planning and implementing their own disclosure laws. It’s estimated that around half of companies that would have fallen within the scope of the SEC’s rules will still face compliance requirements imposed by other jurisdictions. 3

Rowing back on regulations?

In 2025, the rules and rhetoric around ESG are in flux. Having risen rapidly up the corporate agenda in recent years as companies came under pressure to show leadership on environmental protection, social responsibility and good governance, suddenly the outlook for multinationals has become much more uncertain.

How can corporations with global footprints balance the retreat of ESG in some markets with rising regulatory and stakeholder expectations in others?

In some jurisdictions, terms like ESG, sustainability and climate change have become negatively charged, while in others, policy-makers are pressing on with raising ESG standards. At the same time, scrutiny over ESG performance from an influential segment of investors and other stakeholders remains intense, and the value such commitments are judged to deliver is evolving from a compliance-based definition to one tied to operational efficiencies or cost reduction.

In the European Union, regulations around ESG reporting and risk management remain rigorous, despite proposed measures to streamline EU sustainability rules, ease the burden on businesses and boost competitiveness. The “Omnibus Simplification Package” includes steps to harmonize directives relating to corporate sustainability reporting with those on due diligence, reduce the number of companies caught within the reporting requirements and postpone some obligations.

Click here to download the EU’s Omnibus Simplification Package

Against this backdrop, many multinationals today are questioning whether, and to what extent, they should rethink their ESG strategy. Here, we look at how the landscape is changing in different parts of the world and what multinational business leaders need to bear in mind as they chart a course through it.

Regulatory obligations are not the only consideration here. While there are significant reputational benefits from leading on sustainability with customers, staff and other stakeholders in many parts of the world, multinationals are acutely aware that this is no longer the case everywhere. ESG narratives must be consistent across the board, while not coming across as overzealous, or underwhelming, to different audiences.

With this in mind, some companies are choosing to focus on how ESG delivers business value from an operational efficiency or risk mitigation point of view, rather than framing it as a purely compliance exercise, or promoting its “worthiness”. Importantly, when it comes to capital allocation, demand from investors for ESG-focussed opportunities in public and private markets remains strong: not least due to their potential for value creation.7 According to a recent study, 64% of global private equity leaders said they see ESG as a viable value lever.8 No wonder global ESG assets are predicted to be worth as much as $50 trillion by the end of the decade.9 In light of this, shareholder activism is unlikely to abate.

Reference list

(2025, March 27). SEC Votes to End Defense of Climate Disclosure Rules. U.S. Securities and Exchange Commission. https://www.sec.gov/newsroom/press-releases/2025-58 Shonerd, D. (2025, July 8). State Climate Disclosure Laws: All Eyes on California…and Brussels? MultiState. https://www.multistate.us/insider/2025/7/8/state-climate-disclosure-laws-all-eyes-on-californiaand-brussels Ainsworth, W. (2025, July 1). The SEC eliminated climate rules. Other governments are doing the opposite. Harvard Business School, Institute for Business in Global Society, quoting research by non-profit organisation Ceres. https://www.hbs.edu/bigs/federal-climate-rules (2025, March 25). Asia’s Evolving ESG Disclosure Rules: Latest Updates. Compliance and Risk https://www.complianceandrisks.com/blog/asias-evolving-esg-disclosure-rules-latest-updates/ Shihabi, F. The move to mandatory reporting: Survey of Sustainability Reporting 2024. KPMG. https://kpmg.com/sa/en/insights/esg/the-move-to-mandatory-reporting.html#:~:text=The%20UAE%20has%20issued%20a,akin%20to%20other%20regional%20markets (2025, January 25) Jordan stock exchange mandates climate-related disclosures aligned with ISSB standards. XBRL. https://www.xbrl.org/news/jordan-stock-exchange-mandates-climate-related-disclosures-aligned-with-issb-standards/#:~:text=The%20Amman%20Stock%20Exchange%20(ASE,disclosures%20starting%201%20January%202027. Giese, G. and Shah, D. (2025, September 19). ESG Ratings in Global Equity Markets: A Long-Term Performance Review. MSCI https://www.msci.com/research-and-insights/paper/msci-esg-ratings-in-global-equity-markets-a-long-term-performance-review. Quoted here: https://corpgov.law.harvard.edu/2025/07/29/esg-mid-year-update-who-still-cares-and-why-you-should/#1 Wrobel, M. and Fishman, A. (2025, July 29). ESG Mid-Year Update: Who Still Cares, and Why You Should. Harvard Law School Forum on Corporate Governance. https://corpgov.law.harvard.edu/2025/07/29/esg-mid-year-update-who-still-cares-and-why-you-should/#1 Parrish, P. (2024, October 10). Why ESG assets are heading toward $50 trillion despite attacks on ‘woke capitalism’. Fortune. https://fortune.com/2024/10/10/why-esg-assets-grow-despite-attacks-on-woke-capitalism/ (2025, July 17). Corporate Risk Radar Report 2025: Operating in a web of complex risks. Clyde & Co in association with Winmark. https://www.clydeco.com/en/reports/2025/06/crr-operating-in-a-web-of-complex-risks

Richard Power Partner, London

Richard Power is a leading disputes lawyer with over 15 years’ experience in the energy sector. He specialises in complex cross-border and domestic disputes across arbitration, litigation, mediation and other ADR processes. Richard advises on commercial, corporate, regulatory and climate-related disputes, including greenwashing and Energy Charter Treaty claims.

Navigating greenwashing risk in a shifting ESG landscape

Abandoning ESG reporting is a non-starter for some companies

Failure to comply with these laws and regulations can expose a company to fines — for example, CSDDD includes provisions for fines of 5% of a company’s net worldwide turnover for breaches. In August 2024, a UK energy company was fined GBP 25 million by the UK’s energy regulator Ofgem for inaccurately reporting environmental and sustainability data for 2021/2022.

Claims might be contractual, too. Large companies subject to regulations like CSRD and CSDDD are inserting climate-conscious terms in their contracts, requiring counterparties to provide accurate emissions data, backed by warranties and indemnities. Government and local authority requests for proposals (RFPs) often have comprehensive ESG sections; awarded contracts contain warranties regarding the accuracy of information presented. Breaching these warranties can lead not only to contract termination but also exclusion from future public contracts.

Conclusion

Notwithstanding reports to the contrary, there remains a plethora of legislation requiring companies to report on climate-related issues. For example, the EU’s Corporate Sustainability Reporting Directive (CSRD), and forthcoming Corporate Sustainability Due Diligence Directive (CSDDD) have recently been diluted, but still require many large companies to report on environmental and sustainability-related opportunities and risks; carry out and report on due diligence on ESG issues; and put into effect transition plans for climate change mitigation, to align with climate-neutrality. These rules affect large companies headquartered in the EU or with sufficient turnover in the EU even if registered overseas. Moreover, to the extent that they require the reporting and reduction of Scope 3 emissions, companies in the supply chain may be indirectly required to report on their emissions.

This can lead to companies postponing or reconsidering the implementation of net zero and emissions reduction strategies. Adjusting or discontinuing environmental policies can carry legal risk, particularly if the company is subject to regulations that mandate the reporting and reduction of GHG emissions or climate-related risks. But there is potentially greater risk of continuing to report/advertise emissions reduction goals and net zero plans without taking substantive steps toward implementation, as this can expose the company to the financial and reputational risk of greenwashing claims.

Misrepresentations about sustainability or emissions reductions can trigger greenwashing damages claims under many legal systems. Most jurisdictions recognise rights of action for misrepresentation or deceit — especially if these claims induce parties to enter contracts. Misstatements about environmental matters can be misrepresentations as much as misstatements about, say, asset value. Where there is deliberate falsehood, the risk is evident, but companies which report and advertise their emissions reduction plans, but don’t actually implement them, can be exposed to claims where such behaviour is considered reckless, and, in some cases, negligent.

In some jurisdictions, class actions are increasingly being brought against companies that market products as “green” or “sustainable,” such as airlines whose customers allegedly paid premiums based on misleading environmental claims.

ompanies are faced with varied signals regarding greenhouse gas (GHG) emissions reduction

and the adoption of “clean” energy like renewables. In some jurisdictions, years of consumer pressure, government legislation and regulation to encourage or require companies to report on efforts to reduce emissions and net zero initiatives have been followed by changes in policy direction, such as reduced emphasis on emissions reduction measures.

C

Greenwashing — an increasing risk

Green finance and investment further magnify the risks. Preferential loan terms may be tied to achieving specific sustainability targets, and investors increasingly avoid companies deemed pollutive or unsustainable.

Greenwashing can be caught under these laws — even where misleading claims are not explicit. For instance, oil companies might overvalue reserves based on future consumption projections that conflict with stated commitments to reduce emissions.

Under UK law (specifically sections 90 and 90A of the Financial Services and Markets Act), investors have rights to claim losses from reliance on misstatements or omissions in financial disclosures, listing particulars, or prospectuses. Civil liability may arise for companies—and individuals with managerial responsibility—where misleading statements are made in market disclosures, press releases, or financial reports, particularly if such statements are found to be knowing, reckless, or dishonest.

Recent changes in ESG reporting requirements and shifts in regulatory focus may lead some companies into thinking that ESG reporting is of no concern anymore. The truth is far more nuanced, and various legal and reputational risks may still arise from limited or inconsistent approaches to emissions reporting and the implementation of net zero policies, including potential exposure to fines, reputational harm and damages claims.

Many legal frameworks allow for action if investments are made in reliance on misleading financial statements or prospectuses, which now often include environmental data.

Is nuclear energy the key to the energy transition?

Nuclear’s second wind

here is a renewed interest in nuclear power generation given surging demands for energy. As various

governments pledge to commit more to nuclear energy, some have described the current climate as a nuclear renaissance. While this new attitude to nuclear has been touted as having the potential to revolutionise the transition to clean energy, remnants of past scepticism towards nuclear power persist. This article looks at the current state of nuclear power generation and focuses on the impact that the UK Government’s new policy statement on nuclear energy might have on the sector.

T

Small Modular Reactors: Small Modular Reactors (“SMRs”), a subset of Advanced Modular Reactors that have less power capacity than traditional nuclear reactors, are included alongside other large-scale nuclear reactors at power plants. This suggestion is made given SMRs, in comparison to traditional larger reactors, require less initial capital investment, offer scalability to manage growing power needs and can be more easily installed at nuclear power plants.

This is not the first time in modern history that interest in nuclear energy has spiked. The Blair and Bush administrations of the early 2000s invested substantially in nuclear but saw little return from their investment. For example, of the 30 nuclear reactors that were ordered by utility companies in the US under Bush, only four went into construction. Of those four, two were ultimately abandoned after more than USD 9 billion had been spent on their construction.2

Other statistics show that power generated by nuclear energy globally has been declining since the 1990s. From generating 17% of all power in the mid-1990s, only 9% of global power is generated by nuclear energy today. Although more countries have signed the COP28 Declaration to triple nuclear energy capacity by 2050, there are questions as to whether this aspiration is reasonable.

General concerns around Nuclear Energy

Is there potential for a nuclear middle ground?

However, as SMRs are still a relatively new technology, we have not yet seen their results in practice and so the total cost per unit can only be an estimate at this stage. Due to their modular nature, SMRs should have a lower upfront capital cost per unit as they can be mass manufactured and then installed locally on-site. This makes them cheaper to build and install than traditional reactors.4 However, some argue that the per unit cost of a small reactor will actually be higher because they lose out on the benefits of economies of scale.5

Delay: When compared to other sources of renewable energy such as wind, nuclear energy takes a significant amount of time to become fully operational. Each stage of the planning and construction of a nuclear power plant takes ten years to complete, and it then takes a further ten years for the plant to break even on a carbon basis.6

Another issue the power grid in England and Wales faces is that of ‘dunkelflaute.’ This is a German term to describe periods when ‘the wind does not blow and the sun does not shine.’ Whilst a slightly sombre phrase, it highlights the need to find an alternative source of green energy for when unfavourable weather conditions mean wind and solar cannot provide the energy society needs.

As a result, and given the crucial role uranium plays in nuclear power generation, efforts should be focused to ensure that there are sufficient uranium resources in the medium term. 7

As the world revolves more around big tech and the increasing energy requirements that come with it, governments and private companies alike are looking for a clean energy solution.

Therefore, whilst a nuclear power plant takes around 30 years to build and break even on its carbon emissions, a wind turbine would do the same in around 18 months. In this sense, nuclear energy, and specifically SMRs, should be understood as a long-term commitment to climate change, rather than a short-term solution.

Costs: Traditional power plants are notoriously expensive to build and operate. Recent plants, such as the Vogtle reactor in the US and Hinkley Point C in the UK cost an estimated USD 37 billion and GBP 46 billion respectively to get up and running. From this perspective, there is clearly a need for change and it is hoped that deployment of SMRs will provide this. Steps are being taken in this regard, with Rolls Royce recently being chosen as the preferred bidder to work with Great British Energy - Nuclear on its SMR solution at three sites in the UK.3

What’s next?

Department for Energy Security and Net Zero. (2025, February). National Policy Statement for nuclear energy generation (EN-7): Response and new consultation [PDF]. GOV.UK. https://assets.publishing.service.gov.uk/media/67a4e0a68259d52732f6ae08/national-policy-statement-en7-nuclear-consultation.pdf Gunter, L. P. (2021, September 26). The record-breaking failures of nuclear power. Beyond Nuclear International. https://beyondnuclearinternational.org/2021/09/26/the-record-breaking-failures-of-nuclear-power/ and McLeod, H. (2017, August 1). Utilities ditch reactors that launched U.S. nuclear renaissance. Reuters. https://www.reuters.com/article/world/utilities-ditch-reactors-that-launched-us-nuclear-renaissance-idUSKBN1AG22R/ Department for Energy Security and Net Zero. (2025, June 10). Rolls-Royce SMR selected to build small modular nuclear reactors. GOV.UK. https://www.gov.uk/government/news/rolls-royce-smr-selected-to-build-small-modular-nuclear-reactors GOV.UK International Atomic Energy Agency. (n.d.). What are Small Modular Reactors (SMRs)? IAEA. https://www.iaea.org/newscenter/news/what-are-small-modular-reactors-smrs Beyond Nuclear International. (2024, April 10). The record-breaking failures of nuclear power. Financial Times. https://on.ft.com/4jKkjOh Beyond Nuclear International. (2024, April 10). The record-breaking failures of nuclear power. Financial Times. https://on.ft.com/4jKkjOh Austria, V. (2025, April 8). Sufficient uranium resources exist, however investments needed to sustain high nuclear energy growth. IAEA. https://www.iaea.org/newscenter/pressreleases/sufficient-uranium-resources-exist-however-investments-needed-to-sustain-high-nuclear-energy-growth Beyond Nuclear International. (2024, April 10). The record-breaking failures of nuclear power. Financial Times. https://on.ft.com/4jKkjOh Beyond Nuclear International. (2024, April 10). The record-breaking failures of nuclear power. Financial Times. https://on.ft.com/4jKkjOh Water Power Magazine. (2025, May 6). Drax confirms strong outlook, rules out participation in cap and floor scheme for Cruachan II. WaterPower. https://www.waterpowermagazine.com/news/drax-confirms-strong-outlook-rules-out-participation-in-cap-and-floor-scheme-for-cruachan-ii/

Earlier this year, the UK government published an updated draft National Policy Statement for Nuclear Energy Generation (“EN-7”).1 EN-7 emerged from a consultation which assessed the reforms that could be made to the UK’s power grid through the use of nuclear energy, though notably, it extends only to exercise of powers in England and Wales, given devolution of powers to Scottish and Northern Irish Ministers. The consultation closed in April 2025, with a final version of EN-7 expected to be laid before Parliament in Autumn 2025.

National Policy Statement for Nuclear Energy Generation

EN-7 proposed three key changes to the nuclear energy system, with the aim of bringing greater dynamism and flexibility to the nuclear power industry in England and Wales:

Criteria-based approach: The previous National Policy Statement (“EN-6”), imposed a strict criteria system for nuclear power plant development, identifying a set number of locations where nuclear power plants could be developed by a specified date. EN-7 encourages a less constricted development approach by allowing plant developers to select their own sites based on a specified, but less rigid, set of criteria.

Removal of deployment deadline: EN-7 has removed the 2025 deployment deadline that was implemented under EN-6. The UK Government cited the reason for this change as giving more flexibility to nuclear projects, in the hope that the overall development process would be expedited.

It is therefore not surprising that the proposals made under EN-7 are facing scepticism. The main hesitations are:

We will, therefore, not be able to say if SMRs truly represent a low-carbon, lower-cost solution to the energy problem until their capabilities have been tested in practice.

Uranium resources: Long-term investment into nuclear energy raises questions around the suitability of current uranium extraction efforts. According to projections set out in Uranium 2024: Resources, Production and Demand (the latest edition of the uranium reference produced jointly by the OECD Nuclear Energy Agency and the International Atomic Energy Agency), there are sufficient uranium resources to power society’s growth needs through to 2050. However, there are a number of factors which may hinder uranium exploration in the future. These include stricter regulatory processes and technical difficulties in the exploration process.

A suggested solution to ‘dunkelflaute’ is to utilise nuclear power in parallel to other sources of renewable energy, given nuclear energy is constant and does not depend on the same external factors. Some say that SMRs are actually not needed; rather, we should aim to extend the life of old nuclear reactors which would bridge the renewable energy gap for the time being.8

To this end, some countries have already started recommissioning their older nuclear reactors, with Japan reopening 14 plants since the Fukushima disaster in 2011.9

While nuclear power is an option, it remains to be seen whether policymakers will overcome the challenges that come with the nuclear power generation. We must not forget that other alternatives are also competing to balance power systems that are reliant on variable renewable generation. It may be possible that the development of large-scale battery energy storage systems overtake nuclear in the shorter term. In addition, pumped hydro storage might provide other solutions although they have their own cost challenges, as the recent decision by Drax to pause its Cruachan expansion project shows.10 However, it is likely that nuclear energy will play a key role in both domestic and global power generation moving forward.

Victoria Peckett Partner, London

Ross Deuchars Associate, London

Ariana Chis Associate, London

Marianne Anton Partner, London

Ariana is an Associate in the Commercial and Professional Disputes team, specialising in advising accountants, auditors, and insolvency practitioners on professional negligence claims and regulatory investigations. She has experience in commercial litigation, including defending civil claims against auditors, and frequently assists firms with regulatory matters involving bodies such as the FRC and ICAEW. During her training contract, Ariana developed expertise in international arbitration, (re)insurance coverage disputes and commercial litigation, and advised on energy sector disputes and grid connection arrangements.

Ross is an Associate in the Energy, Marine and Natural Resources team. He has represented corporations involved in arbitrations under a variety of rules and in litigation before the English Court. Ross has particular experience in international disputes involving commodities, energy, mining, natural resources, and shipping disputes.

Environmental impact of AI

It is perhaps well known now that the quality of AI depends on the volume of data it has access to, and AI companies are seeking larger and larger data centres to facilitate their programs. These data centres are often located in temperature-controlled buildings that house a wide variety of computing infrastructure, such as servers, data storage drives and network equipment. Further, the use of Large Language Models - machine learning models designed to respond to and generate human language for uses such as response or code generation, language translation or tool use with external applications, to name just a few use-cases - currently requires around ten times more electricity than a standard web search.

The environmental impacts associated with AI use also have implication for businesses, including insurers. Failing to account for the environmental impact of AI can expose businesses to a range of risks.

In the first instance, there is the risk of reputational damage, if stakeholders perceive a lack of environmental responsibility, potentially eroding customer trust and brand value. Secondly, there is a genuine risk of regulatory breaches, as governments and international bodies consider varying environmental reporting and sustainability requirements.

What are the associated risks for businesses

What could be the next steps?

In the EU, the recently introduced AI Act does seek to improve transparency regarding AI’s environmental impact but does not (yet) establish a full set of standards and requirements.

When it comes to creating and using sustainable artificial intelligence, the challenge lies in striking a balance between environmental protection and avoiding the deceleration of AI development.

Does the EU AI Act tackle environmental impacts and related risks?

Finally, businesses may face liability risks if AI-related operations contribute to environmental harm, leading to litigation or regulatory penalties.

What are the environmental impacts?

The overall environmental impact of AI can be divided into two key categories: direct emissions, which includes those from the energy consumed during computing, as well as consumption of other resources such as water, mineral extraction, pollution and the production of e-waste; and indirect emissions, which arise from the related tasks AI has to undertake in order for the tool to be readily available, including the development of AI applications and machine learning.

This calculation does not yet take into account the energy needed to train artificial intelligence or the water consumption in order to cool the data centres.

The environmental impact of AI and its related risks therefore cannot be overlooked.

Environmental regulatory reporting requirements can require businesses to account for environmental impact in a business’ supply chain and while there may not yet be specific language in most regulatory rules that takes account of the impact of AI use, this may change in the future as the environmental impact of AI increasingly becomes the subject of public debate.

Even though the AI Act does not contain reporting obligations and foresees solely limited disclosure, companies need to be aware that the AI Act cannot be seen in isolation. In particular, the EU Energy Efficiency Directive already focusses on energy efficiency in the information and communication technology sector and, in particular, on energy consumption of data centres. Moreover, the non-financial reporting obligations under the EU framework remain of relevance. With the current uncertainty regarding the level and scope of non-financial reporting obligations that the EU will commit to in the long term, it remains crucial for businesses to stay up to date with the regulatory developments in the EU.

rtificial Intelligence (AI) has become an integral part of daily business operations in companies.

While the most common risks of using AI, such as false information or hallucinations, are widely discussed, a more subtle yet equally important risk for businesses to consider is the impact of their usage of AI on the environment.

A

Notably, the EU AI Act requires the providers (being the developer) of general-purpose AI models (in simple terms being AI models which are trained with a large amount of generalized data, and which are capable of performing a wide range of distinct tasks and allowing a variety of applications, GPAI) to maintain technical documentation, including an energy consumption breakdown. Such information can be requested by the AI Office and national competent authorities. This obligation does not extend to “deployers”, that is, those who use GPAI.